How To Develop A Blue Ocean Strategy In A Digital Ecosystem

Back in 2002 I developed a 3 dimensional macro/micro framework based strategy for Multex, one of the earliest and leading online providers of financial information services. The result was to sell themselves to Reuters in a transaction that benefited both companies. 1+8 indeed equaled 12. What I proposed to the CEO was simple. Do “this” to grow to a $500m company or sell yourself. After 3-4 weeks of mulling it over, he took a plane to London and sold his company rather than undertake the “this”.

What I didn’t know at the time was that the “this” was a Blue Ocean Strategy (BOS) of creating new demand by connecting previously unconnected qualitative and quantitative information sets around the “state” of user. For example a portfolio manager might be focused on biotech stocks in the morning and make outbound calls to analysts to answer certain questions. Then the PM goes to a chemicals lunch and returns to focus on industrial products in the afternoon, at which point one of the biotech analysts gets back to him. Problem. The PM’s mental and physical “state” or context is gone. Multex had the ability to build a tool that could bring the PM back to his morning “state” in his electronic workplace. Result, faster and better decisions. Greater productivity, possible performance, definite value.

Sounds like a great story, except there was no BOS in 2002. It was invented in 2005. But the second slide of my 60 slide strategy deck to the CEO had this quote from the author’s of BOS, W.Chan Kim and Renee Mauborgne, of INSEAD, the Harvard Business School of Europe:

“Strategic planning based on drawing a picture…produces strategies that instantly illustrate if they will: stand out in the marketplace, are easy to understand and communicate, and ensure that every employee shares a single visual reference point.”

So you could argue that I anticipated the BOS concept to justify my use of 3D frameworks which were meant to illustrate this entirely new playing field for Multex.

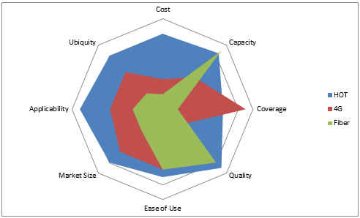

But this piece is less about the InfoStack’s use in business and sports and more about the use of the 4Cs and 4Us of supply and demand as tools within the frameworks to navigate rapidly changing and evolving ecosystems. And we use the BOS graphs postulated by Kim/Mauborgne. The 4Cs and 4Us lets someone introducing a new product, horizontal layer (exchange) or vertical market solution (service integration) figure out optimal product, marketing and pricing strategies and tactics a priori. A good example of this is a BOS I created for a project I am working on in the area of Wifi offload and Hetnet (heterogeneous access networks that can be self-organising) area called HotTowns (HOT). Here’s a picture of it comparing 8 key supply and demand elements across fiber, 4G macro cellular and super saturation offload in a rural community. Note that the "blue area" representing the results of the model can be enhanced on the capacity front by fiber and on the coverage front by 4G.

The same approach can be used to rate mobile operating systems and any other product at a boundary of the infostack or horizontal or vertical solution in the market. We'll do some of that in upcoming pieces.

I met the Godfather of New York Venture capital a few weeks ago and I was talking about an arbitrage opportunity of a lifetime in the communications sector. I started talking about the lack of competition and resulting high prices (which I highlighted last week) brought about by bandwidth being 20-150x overpriced. He just looked at me and said, “bandwidth issue? What bandwidth issue!” It just so happens that his current prize investment is an IPTV application. I just rolled my eyes thinking, “if he only knew!”, remembering what happened to all the web 1.0 companies that ran into the broadband brick wall in 2000.

This statement is symptomatic of the complacency amongst the venture community; those investing billions in the upper layers of the stack. Yet people on Main Street, as evidenced by the Kansas City Fiber video on the Fiber To The Home Council website indicating that 1,000 communities had responded to the contest with over 200,000 people directly involved, know otherwise.

The numbers tell a worse story. Because of the CLEC boom-bust 10-15 years ago, rescission of equal access, failure of muni-WiFi and Wimax and BTOP crowding-out Telecom spending has disconnected from other venture spending over the past decade. Based on overall VC spending telecom spending should be 2-3x greater than it is. Instead it stands 70% below where it was from 1995-2005. It took a while for competition to die, but now it is official!

Venture spending today for the sector, which used to average 15-20% of total VC spending is now down below 5% over the past 3 years. All the other TMT sectors have held nearly constant with overall VC spending.

Everyone should look at these numbers with alarm and reach out to policy makers, academics, trade folks, the venture community and capital markets to make them aware of the dearth of investment as a result of the lack of competition. Now, more than ever contrarian investors should look at the monopoly pricing and realize there is significant profits to be made at all layers of the stack.

Thursday December 19, 2013 will commemorate the 100 year anniversary of the Kingsbury Commitment. There are 528 days remaining. Let's plan something special to observe this tragic moment.

In return for universal service, AT&T was granted a "natural monopoly". The democratic government in the US, one of the few at the time, recognized the virtue of open communications for all and foolishly agreed to Ted Vail's deceptions. Arguably, this one day changed the course of mankind for 50-70 years. Who knows what might have been if we had fostered low-cost communications in the first half of the century?

Anyway, when universal service didn't happen (no sh-t sherlock) the government stepped in to ensure universal service in 1934. So on top of an overpriced monopoly the American public was taxed to ensure 100% of the population got the benefit of being connected. Today, that tax amounts to $15 billion annually to support overpriced service to less than 5% of the population. (Competitive networks have shown how this number gets driven to zero!)

Finally in the early 1980s, after nearly 30 years (the final case started in 1974 and took nearly 9 years) of trying the Department of Justice got a Judge to break up the monopoly into smaller monopolies and provide "equal access" to competitors across the long-distance piece starting and ending at the Class 5 (local switch and calling) boundary. The AT&T monopoly was dead; long live the Baby Bell monopolies! But the divestiture began a competitive long-distance (WAN) digitization "wave" in the 1980s that resulted in, amongst other things:

99% drop in pricing over 10 years

90% touchtone penetration by 1990 vs 20% ROW

Return of large volume corporate traffic via VPN services and growth of switched data intranets

Explosion of free, 800 access (nearly 50% of traffic by 1996)

Over 4 (upwards of 7 in some regions/routes) WAN fiber buildouts

Bell regulatory relief on intralata tolls via expanding calling areas (LATAs)

Introduction of flat-rate local pricing by the Bells

The latter begat the Internet, the second wave of digitization in the early 1990s. The scaling of Wintel driven by the Internet paved the way for low-cost digital cellphones, the third wave of digitization in the late 1990s. (Note, both the data and wireless waves were supported by forms of equal access). By 1999 our economy had come back to the forefront on the global scene and our budget was balanced and we were in a position to pay down our national debt. I expected the 4th and Final Wave of last mile (broadband) digitization to start sometime in the mid to late 2000s. It never came. In fact the opposite happened because of 3 discrete regulatory actions:

1996 Telecom Act

2002 Special Access Deregulation

2004 Rescision of Equal Access and Bell entry into Long Distance (WAN)

Look at the following 6 charts and try not to blink or cry. In all cases, there is no reason why the prices in the US are not 50-70% lower; if not more. We have the scale. We have the usage. We have the industries. We have the technology. We started all the 3 prior waves and should have oriented our vertically integrated service providers horizontally a la the data processing industry to effectively deal with rapid technological change. Finally, we have Moore's and Metcalfe's laws, which argue for a near 60% reduction in bandwidth pricing and/or improved performance annually!

But the government abetted a remonopolization of the sector over the past 15 years.

It's almost a tragedy to be American on this July 4 week. The FCC and the government killed competition brought about by Bill McGowan. But in 2007 Steve Jobs resurrected equal access and competition. So I guess it's great to be American after all! Many thanks to Wall and the Canadian government for these stats.

Since I began covering the sector in 1990, I’ve been waiting for Big Bang II.An adult flick?No, the sequel to Big Bang (aka the breakup of MaBell and the introduction of equal access) was supposed to be the breakup of the local monopoly.Well thanks to the Telecom Act of 1996 and the well-intentioned farce that it was, that didn’t happen and equal access officially died (equal access RIP) in 2005 with the Supreme Court's Brand-X decision vs the FCC. If it died, then we saw a resurrection that few noticed.

I am announcing that Equal Access is alive and well, albeit in a totally unexpected way.Thanks to Steve Jobs’ epochal demands put on AT&T to counter its terrible 2/3G network coverage and throughput, every smartphone has an 802.11 (WiFi) backdoor built-in.Together with the Apple and Google operating systems being firmly out of carriers’ hands and scaling across other devices (tablets, etc…) a large ecosystem of over-the-top (OTT), unified communications and traffic offloading applications is developing to attack the wireless hegemony.

First, a little history. Around the time of AT&T's breakup the government implemented 2 forms of equal access. Dial-1 in long-distance made marketing and application driven voice resellers out of the long-distance competitors. The FCC also mandated A/B cellular interconnect to ensure nationwide buildout of both cellular networks. This was extended to nascent PCS providers in the early to mid 1990s leading to dramatic price declines and enormous demand elasticities. Earlier, the competitive WAN/IXC markets of the 1980s led to rapid price reductions and to monopoly (Baby Bell or ILEC) pricing responses that created the economic foundations of the internet in layers 1 and 2; aka flat-rate or "unlimited" local dial-up. The FCC protected the nascent ISP's by preventing the Bells from interfering at layer 2 or above. Of course this distinction of MAN/LAN "net-neutrality" went away with the advent of broadband, and today it is really just about WAN/MAN fights between the new (converged) ISPs or broadband service providers like Comcast, Verizon, etc... and the OTT or content providers like Google, Facebook, Netflix, etc...

(Incidentally, the FCC ironically refers to edge access providers, who have subsumed the term ISPs or "internet service providers", as "core" providers, while the over-the-top (OTT) messaging, communications, e-commerce and video streaming providers, who reside at the real core or WAN, are referred to as "edge" providers. There are way, way too many inconsistencies for truly intelligent people to a) come up with and b) continue to promulgate!)

But a third form of equal access, this one totally unintentioned, happened with 802.11 (WiFi) in the mid 1990s. The latter became "nano-cellular" in that power output was regulated limiting hot-spot or cell-size to ~300 feet. This had the impact of making the frequency band nearly infinitely divisible. The combination was electric and the market, unencumbered by monopoly standards and scaling along with related horizontal layer 2 data technologies (ethernet), quickly seeded itself. It really took off when Intel built WiFi capability directly into it's Centrino chips in the early 2000s. Before then computers could only access WiFi with usb dongles or cables tethered to 2G phones

Cisco just forecast that 50% of all internet traffic will be generated from 802.11 (WiFi) connected devices.Given that 802.11’s costs are 1/10th those of 4G something HAS to give for the communications carrier.We’ve talked about them needing to address the pricing paradox of voice and data better, as well as the potential for real obviation at the hands of the application and control layer worlds.While they might think they have a near monopoly on the lower layers, Steve Job’s ghost may well come back to haunt them if alternative access networks/topologies get developed that take advantage of this equal access. For these networks to happen they will need to think digital, understand, project and foster vertically complete systems and be able to turn the "lightswitch on" for their addressable markets.

The first quarter global smartphone stats are in and it isn’t even close. With the market growing more than 40%+, Samsung controls 29% of the market and Apple 24%.The next largest, Nokia came in 60-70% below the leaders at 8%, followed by RIMM at 7% and HTC at 5%, leaving the scraps (28%) to Sony, Motorola, LG, ZTE. They've all already lost on the scale front; they need to change the playing field.

While this spread sounds large and improbable, it is not without historical precedent.In 1914, just 6 years after its introduction the Ford Model T commanded 48% market share. Even by 1923 Ford still had 40% market share.2 years later the price stood at $260, which was 30% of the original model in 1908, and less than 10% what the average car cost in 1908; sounds awfully similar to Moore’s law and the pricing of computer/phone devices over the past 30 years.Also, a read on the Model T's technological and design principles sounds a lot like pages taken out of the book of Apple.Or is it the other way around?

Another similarity was Ford’s insistence on the use of black beginning in 1914.Over the life of the car 30 different variations of black were used!The color limitation was a key ingredient in the low cost as prior to 1914, the company used blue, green, red and grey.Still 30 variations of black (just like Apple’s choice of white and black only and take it or leave it silo-ed product approach) is impressive and is eerily similar to Dutch Master Frans Hals’ use of 27 variations of Black, so inspirational to Van Gogh. Who says we can’t learn from history.

Ford’s commanding lead continued through 1925 even as competitors introduced many new features, designs and colors.Throughout, Ford was the price leader, but when the end came for that strategy it was swift. Within 3 years the company had completely changed its product philosophy introducing the Model A (with 4 colors and no black) and running up staggering losses in 1927-28 in the process.But the company saw market share rebound from 30% to 45% in the process; something that might have been maintained for a while had not the depression hit.

The parallels between the smartphone and automobile seem striking. The networks are the roads.The pricing plans are the gasoline.Cars were the essential component for economic advancement in the first half of the 20th century, just as smartphones are the key for economic development in the first half of the 21st century. And now we are finding Samsung as Apple's GM; only the former is taking a page from both GM and Ford's histories. Apple would do well to take note.

So what are the laggards to do to make it an even race?We don’t think Nokia’s strategy of coming out with a different color will matter.Nor do we think that more features will matter.Nor do we think it will be about price/cost.So the only answer lies in context; something we have raised in the past on the outlook for the carriers.More to come on how context can be applied to devices. Hint, I said devices, not smartphones. We'll also explore what sets Samsung and Apple apart from the rest of the pack.

I love talking to my smartphone and got a lot of grief for doing so from my friends last summer while on vacation at the shore.“There’s Michael talking crazy, again,” as I was talking TO my phone, not through it.“Let’s ask Michael to ‘look’ that up! Haha.”And then Siri came along and I felt vindicated and simultaneously awed.The latter by Apple’s (AAPL, OCF = 6.9x) marketing and packaging prowess; seemingly they had trumped Google/Android (GOOG, OCF = 9.6x) yet again.Or had they?What at first appeared to be a marketing coup may become Tim Cook’s Waterloo and sound a discordant note for Nuance (NUAN, OCF = 31x).At its peak in early February NUAN hit a high of 42x OCF, even as Apple stood at 8.2x.

The problem for Apple and Nuance in the short term is that the former is doubling down on its Siri bet with a brand new round of ads by well-known actors, such as Samuel L. Jackson and Zooey Deschanel.Advertising pundits noted this radical departure for a company that historically shunned celebrities. Furthermore, with two (NY and LA) class action suits against it and financial pundits weighing in on the potential consumer backlash Apple could have a major Siri migraine in the second half.Could it be as big as Volvo’s advertising debacle 20 years ago; a proverbial worm in the apple?Time will tell.

The real problem isn’t with Apple, the phone or Siri and its technology DNA, rather the problem lies with bandwidth and performance of the wireless networks.Those debating whether Siri is a bandwidth hog are missing the point.Wireless is a shared spectrum.The more people who are on the same spectrum band, the less bandwidth for each user and the higher the amount of noise.Both are bad for applications like Siri and Android’s voice recognition since they talk with processors in the cloud (or WAN).Delays and missed packets have a serious impact on comprehension, translation and overall responsiveness.Being a frequent user of Google’s voice-rec which has been around since August, 2010, I know when to count on voice-rec by looking at the wifi/3G/2G indicator and the number of bars.But do others know this and will the focus on Siri's performance shift to the network?Time will tell.

The argument that people know voice-rec is new and still in beta probably won’t cut it either.I am puzzled why major Apple fanboys don’t perceive it as a problem, not even making it on this list of 5 critical product issues for the company to address.But maybe that’s why companies like Apple are successful; they push the envelope.In the 1990s I said to the WAN guys (Sprint, et al) that they would have the advantage over the baby bells because the “cloud” or core was more important than the edge.The real answer, which Apple fully understands, is that the two go hand in hand.For Sprint (S, OCF = 3.2x) there were too many variables they couldn’t control, so they never rolled out voice recognition on wired networks.They probably should have taken the chance.Who knows, the “pin-drop” company could have been a whole lot better off!

A natural opposite for "siri" for the droid crowd would be an "Eliza", based on Audrey Hepburn's famous 'The Rain in Spain' character. Eliza is the name of a company specializing in voice-rec healthcare apps and also a 1960s AI psychotherapy program.

Previously we have written about “being digital” in the context of shifting business models and approaches as we move from an analog world to a digital world.Underlying this change have been 3 significant tsunami waves of digitization in the communications arena over the past 30 years, underappreciated and unnoticed by almost all until after they had crashed onto the landscape:

The WAN wave between 1983-1990 in the competitive long-distance market, continuing through the 1990s;

The Data wave, itself a direct outgrowth of the first wave, began in the late 1980s with flat-rate local dial-up connections to ISPs and databases anywhere in the world (aka the Web);

The Wireless wavebeginning in the early 1990s and was a direct outgrowth of the latter two.Digital cellphones were based on the same technology as the PCs that were exploding with internet usage.Likewise, super-low-cost WAN pricing paved the way for one-rate, national pricing plans. Prices dropped from $0.50-$1.00 to less than $0.10. Back in 1996 we correctly modeled this trend before it happened.

Each wave may have looked different, but they followed the same patterns, building on each other.As unit prices dropped 99%+ over a 10 year period unit demand exploded resulting in 5-25% total market growth.In other words, as ARPu dropped ARPU rose; u vs U, units vs Users.Elasticity.

Yet with each new wave, people remained unconvinced about demand elasticity.They were just incapable of pivoting from the current view and extrapolating to a whole new demand paradigm.Without fail demand exploded each time coming from 3 broad areas: private to public shift, normal price elasticity, and application elasticity.

Private to Public Demand Capture.Monopolies are all about average costs and consumption, with little regard for the margin.As a result, they lose the high-volume customer who can develop their own private solution.This loss diminishes scale economies of those who remain on the public, shared network raising average costs; the network effect in reverse.Introducing digitization and competition drops prices and brings back not all, but a significant number of these private users.Examples we can point to are private data and voice networks, private radio networks, private computer systems, etc…that all came back on the public networks in the 1980s and 1990s.Incumbents can’t think marginally.

Normal Price Elasticity.As prices drop, people will use more.It gets to the point where they forget how much it costs, since the relative value is so great.One thing to keep in mind is that lazy companies can rely too much on price and “all-you-can-eat” plans without regard for the real marginal price to marginal cost spread.The correct approach requires the right mix of pricing, packaging and marketing so that all customers at the margin feel they are deriving much more value than what they are paying for; thus generating the highest margins.Apple is a perfect example of this.Sprint’s famous “Dime” program was an example of this.The failure of AYCE wireless data plans has led wireless carriers to implement arbitrary pricing caps, leading to new problems.Incumbents are lazy.

Application Elasticity. The largest and least definable component of demand is the new ways of using the lower cost product that 3rd parties drive into the ecosystem.They are the ones that drive true usage via ease of use and better user interfaces.Arguably they ultimately account for 50% of the new demand, with the latter 2 at 25% each.With each wave there has always been a large crowd of value-added resellers and application developers that one can point to that more effectively ferret out new areas of demand.Incumbents move slowly.

Demand generated via these 3 mechanisms soaked up excess supply from the digital tsunamis. In each case competitive pricing was arrived at ex ante by new entrants developing new marginal cost models by iterating future supply/demand scenarios. It is this ex ante competitive guess, that so confounds the rest of the market both ahead and after the event. That's why few people recognize that these 3 historical waves are early warning signs for the final big one.The 4th and final wave of digitization will occur in the mid-to-last mile broadband markets. But many remain skeptical of what the "demand drivers" will be. These last mile broadband markets are monopoly/duopoly controlled and have not yet realized price declines per unit that we’ve seen in the prior waves. Jim Crowe of Level3 recently penned a piece in Forbes that speaks to this market failure. In coming posts we will illustrate where we think bandwidth pricing is headed, as people remain unconvinced about elasticity, just as before. But hopefully the market has learned from the prior 3 waves and will understand or believe in demand forecasts if someone comes along and says last mile unit bandwidth pricing is dropping 99%. Because it will.

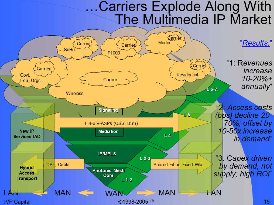

I first started using clouds in my presentations in 1990 to illustrate Metcalfe’s Law and how data would scale and supersede voice. John McQuillan and his Next Gen Networks (NGN) conferences were my inspiration and source. In the mid-2000s I used them to illustrate the potential for a world of unlimited demand ecosystems: commercial, consumer, social, financial, etc…Cloud computing has now become a part of everyday vernacular.The problem is that for cloud computing to expand the world of networks needs to go flat, or horizontal, as in this complex looking illustration to the left.

This is a static view.Add some temporality and rapidly shifting supply/demand dynamics and the debate begins as to whether the system should be centralized or decentralized.Yes and no.There are 3 main network types:hierarchical, centralized and fully distributed (aka peer to peer).None fully accommodate metcalfe’s, moore’s and zipf’s laws.Network theory needs to capture the dynamic of new service/technology introduction that initially is used by a small group, but then rapidly scales to many.Processing/intelligence initially must be centralized but then traffic and signaling volumes dictate pushing the intelligence to the edge. The illustration to the right begins to convey that lateral motion in a flat, layered architecture, driven by the 2-way, synchronous nature of traffic; albeit with the signalling and transactions moving vertically up and down.

But just as solutions begin to scale, a new service is borne superseding the original.This chaotic view from the outside looks like an organism in constant state of expansion then collapse, expansion then collapse, etc…

A new network theory that controls and accounts for this constant state of creative destruction* is Centralized Hierarchical Networks (CHNs) CC.A search on google and duckduckgo reveals no known prior attribution, so Information Velocity Partners, LLC (aka IVP Capital, LLC) both lays claim and offers up the term under creative commons (CC).I actually coined the CHN term in 2004 at a Telcordia symposium; now an Ericsson subsidiary.

CHN theory fully explains the movement from mainframe to PC to cloud. It explains the growth of switches, routers and data centers in networks over time. And it should be used as a model to explain how optical computing/storage in the core, fiber and MIMO transmission and cognitive radios at the edge get introduced and scaled. Mobile broadband and 7x24 access /syncing by smartphones are already beginning to reveal the pressures on a vertically integrated world and the need to evolve business models and strategies to centralized hierarchical networking.

*--interesting to note that creative destruction was original used in far-left Marxist doctrine in the 1840s but was subsumed into and became associated with far-right Austrian School economic theory in the 1950s. Which underscores my view that often little difference lies between far-left and far-right in a continuous circular political/economic spectrum.

Is reality mimicking art?Is Android following the script from Genesis’ epochal hit Land of Confusion? Is it a bad dream on this day that happens once every four years?Yes, yes, and unfortunately no.Before I go into a litany of ills besetting the Android market and keeping Apple shareholders very happy, two points: a) I have an HTC Incredible and am a Droid fan, and b) the 1986 hit parodied superpower conflict and inept decisions by global leaders but presaged the fall of the Berlin Wall and 20+ years of incredible growth, albeit with a good deal of 3rd world upheaval in the Balkans, Mid-east, and Africa.So maybe there is hope that out of the current state a new world order will arise as the old monopolies are dismantled.

Apple clearly has the digital formula right at present; simplicity, ease of use, performance, and yet, at the same time unlimited choice and customization.Contrast that with this parody from SNL of Verizon and 4G/3G/2G/noG and the Samsung Superbowl Ad portraying a wild party.The result is a disturbing trend if you are an Android phone lover. The ecosystem’s rate of new technology adoption is slowing down even if better technology is being made as consumers are clearly confused. In the tablet market there is even a greater disparity, with Android tablets hardly making a dent in Apple's share.

Yesterday Eric Schmidt prognosticated at MWC a world where more is better and cheaper; which may be good for Google but not necessarily the best thing for anyone else in the Droid ecosystem, including consumers.Yet, at the same time Apple managed to steal the show with its iPad3 announcement.Contrast this with HTC rolling out some awesome phones that will not be available in the US this year because their chip doesn't support 4G.

The answer is not better technology, but better ecosystems.The Droid device vendors should realize this and build a layer of software and standards above Google/ICS to facilitate interoperability across silos (at the individual, device and network level); instead of just depreciating their hardware value by competing on price and features many people do not want. They can then collectively win in residual transaction streams (like collectively synching back to a dropbox) like Apple.

Examples of these include standardization and interoperability of free or subsidized wifi offload, over the top messaging, voice and other solutions and the holy grail, mobile payments. Companies like CloudFoundry allows for cross Cloud application infrastructure support, with AppFog and Iron Foundry are pursuing these approaches individually. But just think what would happen if Samsung, HTC, LG and Motorola were to band together and coordinate these approaches and develop very low cost balanced payment systems within the Droid ecosystem to promote interoperability and cooperation, counteract Google and restore some sanity to the market. Carriers (um battleships?) will not be able to stop this effort and may even welcome it just as the music industry opened its arms to Apple.

Apple hasn’t been an innovator so much as a great design company that understands big market opportunities and what the customer wants. The result is an established order that other industries and their customers clearly prefer. Millenials are too young to know Land of Confusion, but the current decision makers in the Droid ecosystem do and so they should take a lesson from history on this Leap Day.Hopefully we’ll wake up in 4 years and there will be a wonderful new world order. Oh, and a Happy 4 Birthdays to everyone present and past who was born on this day.

Wireless service providers (WSPs) like AT&T and Verizon are battleships, not carriers.Indefatigable...and steaming their way to disaster even as the nature of combat around them changes.If over the top (OTT) missiles from voice and messaging application providers started fires on their superstructures and WiFi offload torpedoes from alternative carriers and enterprises opened cracks in their hulls, then Dropbox bombs are about to score direct hits near their water lines.The WSPs may well sink from new combatants coming out of nowhere with excellent synching and other novel end-user enablement solutions even as pundits like Tomi Ahonen and others trumpet their glorious future.Full steam ahead.

Instead, WSP captains should shout “all engines stop” and rethink their vertical integration strategies to save their ships.A good start might be to look where smart VC money is focusing and figure out how they are outfitted at each level to defend against or incorporate offensively these rapidly developing new weapons.More broadly WSPs should revisit the WinTel wars, which are eerily identical to the smartphone ecosystem battles, and see what steps IBM took to save its sinking ship in the early 1990s.One unfortunate condition might be that the fleet of battleships are now so widely disconnected that none have a chance to survive.

The bulls on Dropbox (see the pros and cons behind the story) suggest that increased reliance on cloud storage and synching will diminish reliance on any one device, operating system or network.This is the type of horizontalization we believe will continue to scale and undermine the (perceived) strength of vertical integration at every layer (upper, middle and lower).Extending the sea battle analogy, horizontalization broadens the theatre of opportunity and threat away from the ship itself; exactly what aircraft carriers did for naval warfare.

Synching will allow everyone to manage and tailor their “states”, developing greater demand opportunity; something I pointed out a couple of months ago.People’s states could be defined a couple of ways, beginning with work, family, leisure/social across time and distance and extending to specific communities of (economic) interest.I first started talking about the “value of state” as Chief Strategist at Multex just as it was being sold to Reuters.

Back then I defined state as information (open applications, communication threads, etc...) resident on a decision maker’s desktop at any point in time that could be retrieved later.Say I have multiple industries that I cover and I am researching biotech in the morning and make a call to someone with a question.Hours later, after lunch meetings, I am working on chemicals when I get a call back with the answer.What’s the value of bringing me back automatically to the prior biotech state so I can better and more immediately incorporate and act on the answer?Quite large.

Fast forward nearly 10 years and people are connected 7x24 and checking their wireless devices on average 150x/day.How many different states are they in during the day?5, 10, 15, 20?The application world is just beginning to figure this out.Google, Facebook, Pinterest and others are developing data engines that facilitate “free access” to content and information paid for by centralized procurement; aka advertising.Synching across “states” will provide even greater opportunity to tailor messages and products to consumers.

Inevitably those producers (advertisers) will begin to require guaranteed QoS and availability levels to ensure a good consumer experience. Moreover, because of social media and BYOD companies today are looking at their employees the same way they are looking at their consumers.The overall battlefield begins to resemble the 800 and VPN wars of the 1990s when we had a vibrant competitive service provider market before its death at the hands of the 1996 Telecom Act (read this critique and another that questions the Bell's unnatural monopoly).Selling open, low-cost, widely available connectivity bandwidth into this advertising battlefield can give WSPs profit on every transaction/bullet/bit across their network.That is the new “ship of state” and taking the battle elsewhere.Some call this dumb pipes; I call this a smart strategy to survive being sunk.

market and Apple 24%.

market and Apple 24%. 10% what the average car cost in 1908; sounds awfully similar to Moore’s law and the pricing of computer/phone devices over the past 30 years.

10% what the average car cost in 1908; sounds awfully similar to Moore’s law and the pricing of computer/phone devices over the past 30 years. its product philosophy introducing

its product philosophy introducing  will matter.

will matter. as I was talking TO my phone, not through it.

as I was talking TO my phone, not through it.

e baby bells because the “cloud” or core was more important than the edge.

e baby bells because the “cloud” or core was more important than the edge. context of shifting business models and approaches as we move from an analog world to a digital world.

context of shifting business models and approaches as we move from an analog world to a digital world. resellers and application developers that one can point to that more effectively ferret out new areas of demand.

resellers and application developers that one can point to that more effectively ferret out new areas of demand. I first started using clouds in my presentations in 1990 to illustrate Metcalfe’s Law and how data would scale and supersede voice.

I first started using clouds in my presentations in 1990 to illustrate Metcalfe’s Law and how data would scale and supersede voice. theory needs to capture the dynamic of new service/technology introduction that initially is used by a small group, but then rapidly scales to many.

theory needs to capture the dynamic of new service/technology introduction that initially is used by a small group, but then rapidly scales to many. and unfortunately no.

and unfortunately no. Apple clearly has the

Apple clearly has the  is better and cheaper; which may be good for Google but not necessarily the best thing for anyone else in the Droid ecosystem, including consumers.

is better and cheaper; which may be good for Google but not necessarily the best thing for anyone else in the Droid ecosystem, including consumers.

providers started fires on their superstructures and WiFi offload torpedoes from alternative carriers and enterprises opened cracks in their hulls, then

providers started fires on their superstructures and WiFi offload torpedoes from alternative carriers and enterprises opened cracks in their hulls, then