|

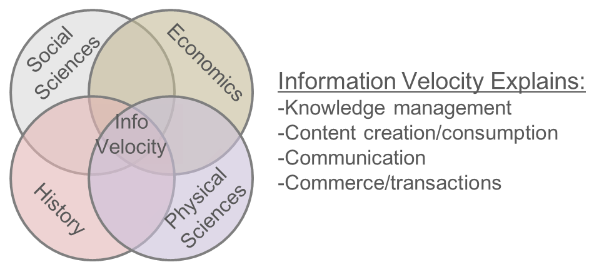

Information Velocity

“The rate at which data is created, transmitted, processed, stored and repurposed − has been the key determinant of economic growth, innovation and competitive advantage throughout history, but there has been no point in time more dependent on information velocity than today. In the TMT and ICT industries there are many barriers to be removed and white space opportunities to be captured by thinking outside the box with blue-ocean strategies.” - Michael Elling, CEO/Founder, IVP Capital

The relationship between and value of networks is summed up in this simple example which is almost entirely missing from today's understanding of the business models of networks: "If network A has 1 million users and network B has 1000 users, the value of network B to network A is up to 2000x greater with terminating settlement than with just bill and keep, or no settlement. Therefore it is in A’s interest to “fund” B’s network via a terminating settlement to capture and retain that increased value. This is also known as the network effect or metcalfe's law."

IVP Capital helps clients remove barriers to facilitate faster velocity of information, seize opportunities and achieve ROI

|

|

|

|

Analytics

Strategy

Capital | |

|  |

|

|

Objective

Thorough

Forecasts | |

| |

|

|

We are in the early stages of a very large strategic cycle, driven by the mutally dependent cloud (click here for background) and smartphone (click here for background). This "4th Wave" of digitization will feed on and be bigger than the Wintel/Internet and digital wireless cycles in the 1980s-90s--along with the separation of MaBell in 1983 and resulting competition in the WAN--which we refer to as the three prior waves of digitization that took place during the 1980s-00s. Each of these waves was marked by shifts from analog to digital pricing, with 99%+ price declines over 10 years offset by:

- pricing elasticity

- application elasticity

- private to public demand shifts

In each wave, revenues grew and new economies developed that few could perceive or predict in the late 1970s. We see the 4th wave--a broadband IP Tsunami crashing on the traditional service providers and other traditional "analog" business models (health, government, education, transportation, manufacturing)--resembling the 3 prior waves. IVP uses the blueprints and lessons (click here for background) learned in supply and demand from those first 3 waves to assist clients in riding out and navigating this cycle.

|

|

The feed has not been setup

|